Key Takeaways on Updated Main Street Lending Program Materials

On May 27, 2020, the Federal Reserve Bank of Boston released updated Frequently Asked Questions (FAQs) and certain operational documents with respect to the Main Street Lending Program. The additional materials provide clarification on existing terms, add new requirements, include certain form documents to be used by borrowers and lenders, and give further guidance on the operation of the program. However, the FAQs and materials did not provide any form of loan application or timing of the program rollout.

Among the form documents are a Participation Agreement (which governs the purchase of the participation interest), Lender Registration Certifications and Covenants, a Servicing Agreement (which governs the administration of the participation and delivery of certain financial information), a Co-Lender Agreement (which would allow a bi-lateral facility to be converted into a multi-lender facility if there is an elevation of a participation interest), Lender Transaction Specific Certifications and Covenants, and Borrower Certifications and Covenants.

The updates expand the reach of the affiliation rules: affiliates of borrowers are now aggregated for purposes of (i) determining the Main Street loan facility that is available to a borrower, and (ii) the maximum loan size that a borrower may receive. Portfolio companies of private equity funds are not excluded from the Main Street Lending Program on a de facto basis. However, this expansion of the affiliation rules could impact the amount of Main Street loans that portfolio companies of private equity funds are able to receive.

Other notable changes are: (1) a no adequate credit available certification that is required from the borrower, (2) a new Collateral Coverage Ratio requirement for the Priority Loan Facility, (3) updated guidance on the security requirements for the Priority Loan Facility and Expanded Loan Facility, (4) clarifications on the methodology used to calculate EBITDA and permissible repayments of other debt, and (5) details on the rights the SPV will have via its participation, including specific voting rights and rights to elevate and/or transfer its participation.

The updated materials are available at the Federal Reserve Bank of Boston’s website by clicking here.

This bulletin briefly describes the key takeaways on the updated Main Street Lending Program materials. Alongside this bulletin, we have updated our easy-to-digest chart setting forth the high-level terms of the Main Street Lending Program. We note that this is current as of June 3, 2020 and adjustments to the program may be made in the future.

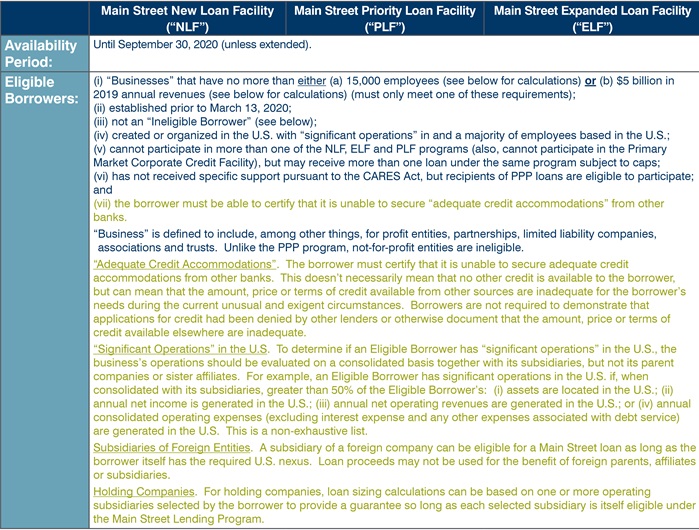

Click the image below to view the chart in full.

1. Expansion of Affiliation Rules: Affiliates will be aggregated with an Eligible Borrower not only for purposes of the maximum employee count (15,000) and maximum revenue ($5 billion) eligibility calculations, but now also will be aggregated for purposes of (i) determining the Main Street loan facility that is available to an Eligible Borrower, and (ii) the maximum loan size that an Eligible Borrower may receive.

- Available Loan Facility. An affiliated group of businesses can participate in only one Main Street facility, and cannot participate in both a Main Street facility and the Primary Market Corporate Credit Facility (PMCCF). For example, if an Eligible Borrower’s affiliate has participated in the New Loan Facility or has a pending application to participate in the New Loan Facility, then the Eligible Borrower would only be able to participate in the New Loan Facility and would be prohibited from participating in the Priority Loan Facility and Expanded Loan Facility.

- Maximum Loan Size. The maximum loan amounts that apply to an individual Eligible Borrower also apply to an Eligible Borrower and its affiliates in the aggregate. An Eligible Borrower’s maximum loan size is limited by its own leverage level, the leverage level of the affiliated group on a consolidated basis, and the size of any loan extended to other affiliates in the group. For example, in the case of the New Loan Facility, a potential borrower’s maximum loan amount would be the lesser of:

(a) $25 million (less any amount extended to an affiliate of the Eligible Borrower under the New Loan Facility);

(b) 4x 2019 adjusted EBITDA of the Eligible Borrower minus Eligible Borrower’s existing outstanding and undrawn available debt; and

(c) 4x 2019 adjusted EBITDA of the Eligible Borrower and its affiliates on a consolidated basis minus existing outstanding and undrawn available debt of the Eligible Borrower and its affiliates on a consolidated basis.

The affiliation test for maximum loan sizing purposes is the same one used for the maximum employee and revenue eligibility calculations. The affiliation test applies to private equity-owned businesses in the same manner as any other business subject to outside ownership or control. It is noted that the SBA affiliation exceptions in 13 CFR 121.103(b) apply to the Main Street Lending Program, including the exception for business concerns owned in whole or substantial part by investment companies licensed under the Small Business Investment Act of 1958, as amended.

VEDDER OBSERVATION: Although portfolio companies of private equity funds are not excluded from the Main Street Lending Program, this expansion of the affiliation rules could impact the amount of Main Street loans that portfolio companies of private equity funds are able to receive. However, we note that the Forms of Lender Transaction Specific Certifications and Covenants state that affiliates are included in loan sizing calculations “… if one or more of the Borrower’s affiliates previously participated, or has applied to participate, in the Facility ….” While the FAQs are not clear on this point, if a potential borrower’s affiliates have not applied for or participated in the Main Street Lending Program, then it is possible that affiliates need not be included in loan sizing calculations. Another open question is whether only those affiliates that apply for or participate in the Main Street Lending Program should be included in the loan sizing calculations (rather than all affiliates).

2. Other Eligibility Requirements:

- No Adequate Credit Elsewhere. The borrower must certify that it is unable to secure adequate credit accommodations from other banks. This does not necessarily mean that no other credit is available to the borrower, but can mean that the amount, price or terms of credit available from other sources are inadequate for the borrower’s needs during the current unusual and exigent circumstances. Borrowers are not required to demonstrate that applications for credit had been denied by other lenders or otherwise document that the amount, price or terms of credit available elsewhere are inadequate.

- Subsidiaries of Foreign Entities. A subsidiary of a foreign company can be eligible for a Main Street loan as long as the borrower itself has the required U.S. nexus. Loan proceeds may not be used for the benefit of foreign parents, affiliates or subsidiaries.

- Significant Operations. To determine if an Eligible Borrower has “significant operations” in the U.S., the business’s operations should be evaluated on a consolidated basis together with its subsidiaries, but not its parent companies or sister affiliates. For example, an Eligible Borrower has significant operations in the U.S. if, when consolidated with its subsidiaries, greater than 50% of the Eligible Borrower’s: (i) assets are located in the U.S.; (ii) annual net income is generated in the U.S.; (iii) annual net operating revenues are generated in the U.S.; or (iv) annual consolidated operating expenses (excluding interest expense and any other expenses associated with debt service) are generated in the U.S. This is a non-exhaustive list.

- Private Equity. While portfolio companies of private equity funds may be eligible for Main Street loans, private equity funds themselves are ineligible.

- Holding Companies. For holding companies, loan sizing calculations can be based on one or more operating subsidiaries selected by the borrower to provide a guarantee so long as each selected subsidiary is itself eligible under the Main Street Lending Program.

3. Expanded Loan Facility Updates:

- Eligible Lender Timing. The Eligible Lender is not required to have been the same Eligible Lender that originally extended the loan underlying an upsized tranche. However, the Eligible Lender must have purchased the interest in the underlying loan as of December 31, 2019, and the Eligible Lender must have assigned an internal risk rating to the underlying loan equivalent to a “pass” in the FFIEC’s supervisory rating system as of that date. Also, if an existing loan was originated after December 31, 2019, the Eligible Lender should use the internal risk rating given to that loan at origination to determine whether the loan is eligible for upsizing under the Expanded Loan program.

- 35% Prong of Loan Sizing Test. If the upsized tranche is part of a secured loan, then all secured debt for borrowed money that has not been made junior in priority through contractual subordination should be included in the 35% calculation regardless of value or type of collateral. If the upsized tranche is part of an unsecured loan, then all unsecured debt for borrowed money that has not been made junior in priority through contractual subordination should be included in the 35% calculation.

4. Priority Loan Facility Update:

- New Collateral Coverage Ratio Requirement. If the Priority Loan is secured, then the Collateral Coverage Ratio (i.e., the aggregate value of any relevant collateral, including the pro rata value of any Shared Collateral, divided by the outstanding aggregate principal amount of the relevant debt) for the Priority Loan at the time of its origination must be either (i) at least 200% or (ii) not less than the aggregate Collateral Coverage Ratio for all of the Borrower’s other secured Loans or Debt Instruments (other than mortgage debt).

5. Security Updates for Priority Loan Facility and Expanded Loan Facility:

- The Priority Loan and Expanded Loan must be secured if, at the time of origination, the Eligible Borrower has any other secured Loans or Debt Instruments (i.e., debt for borrowed money and all obligations evidenced by bonds, debentures, notes, loan agreements or other similar instruments, and all guarantees of the foregoing), other than mortgage debt.

- In the case of the Expanded Loan Facility, if the underlying credit facility includes both term loan tranche(s) and revolver tranche(s), the upsized tranche needs to share collateral on a pari passu basis with the term loan tranche(s) only.

- The lien of the Eligible Lender in any Shared Collateral (i.e., any collateral security for the eligible loan that is also collateral security for any of the borrower’s or guarantors’ other Loans or Debt Instruments (other than mortgage debt)) must be senior to or pari passu with the lien on Shared Collateral that secures any of the borrower’s other Loans or Debt Instruments (other than mortgage debt), including any other tranches in respect of the underlying loan in the case of the Expanded Loan Facility.

- The Priority Loan need not share in all of the collateral that secures the Eligible Borrower’s other Loans or Debt Instruments.

- The loan documents for the Priority Loan Facility and the Expanded Loan Facility must contain a lien covenant or negative pledge that is of the type – and contains exceptions, limitations, carve-outs, baskets, materiality thresholds, and qualifiers – that are consistent with those used by the Eligible Lender in its ordinary course lending to similarly situated borrowers. In the case of the Expanded Loan Facility, any lien covenant that was negotiated in good faith prior to April 24, 2020, as part of any underlying loan, is sufficient to satisfy this requirement.

6. EBITDA Calculations:

- If an Eligible Lender has used multiple EBITDA adjustment methods with respect to the Eligible Borrower or similarly situated borrowers (e.g., one for use within a credit agreement and one for internal risk management purposes), the Eligible Lender should choose the most conservative method (no cherry-picking), and must use a method used recently, but prior to April 24, 2020. The Eligible Lender should document the rationale for its selection of an adjusted EBITDA methodology.

- In the case of the Expanded Loan Facility, if EBITDA was not calculated or used when originating the loan underlying the upsized tranche, the Eligible Borrower’s adjusted EBITDA must be calculated using a methodology that the Eligible Lender has required to be used in other contexts for the Eligible Borrower or, if there is no such calculation, for similarly situated borrowers.

- Similarly situated borrowers are borrowers in similar industries with comparable risk and size characteristics. Eligible Lenders should document their process for identifying similarly situated borrowers when they originate a New Loan or Priority Loan.

7. Fees: Eligible Lenders are not permitted to charge Eligible Borrowers any additional fees beyond the fees described in the Main Street Lending Program, except de minimis fees for services that are customary and necessary, such as appraisal and legal fees. Eligible Lenders should not charge servicing fees to Eligible Borrowers.

8. Loan Documentation:Eligible Lenders should use their own standard loan documents which should be substantially similar (except for necessary changes to accommodate the requirements of the Main Street Lending Program), including with respect to covenants, to the loan documents used in its ordinary course lending to similarly situated borrowers (in terms of industry and risk and size characteristics). There are certain covenants that are required to be included in the loan documents, including with respect to mandatory prepayments, cross-acceleration and financial reporting (samples of which have been provided).

9. Repayments:

- Repaying Other Debt. Eligible Borrowers are generally prohibited from repaying other debt until the Main Street loan is repaid in full, unless the principal or interest payment is “mandatory and due,” meaning (a) on the future date upon which they were scheduled to be paid as of April 24, 2020 or (b) upon the occurrence of an event that automatically triggers mandatory prepayments under a contract for indebtedness that the Eligible Borrower executed prior to April 24, 2020, except that any such prepayments triggered by the incurrence of new debt can only be paid if they are de minimis or, in the case of Priority Loans, at the time of origination.

- Mandatory Prepayment of Existing Debt. If an Eligible Borrower has an existing debt arrangement that requires prepayment of more than a de minimis amount upon the incurrence of new debt, the Eligible Borrower cannot receive a New Loan or Expanded Loan unless such requirement is waived or reduced to a de minimis amount by the relevant creditor.

10. SPV Participation:

- Voting. The SPV will have voting rights with respect to items that are customary “sacred rights” and certain other items that are specific to the Main Street Lending Program, such as waivers of conditions precedent to closing, amendments to certain borrower eligibility certifications and covenants, amendments to certain periodic financial reporting, greater restrictions on lender assignability, adverse effect on participated loans that would be disproportionate, and certain actions relating to the required cross-acceleration provisions.

- Elevation of SPV Participation. The SPV can generally elevate its participation in the loan into an assignment without the consent of the Eligible Lender and Eligible Borrower in the following circumstances: (i) if the Eligible Borrower fails to make a payment and the applicable grace period expires; (ii) if the Eligible Borrower or Eligible Lender is subject to bankruptcy or insolvency proceedings; (iii) automatically, if the Eligible Lender would allow any portion of the underlying loan to be forgiven; and (iv) if required by law.

- Sale of SPV Participation. The SPV is generally permitted to sell its participation (without elevating) only with the contemporaneous consent of the Eligible Lender. In addition, it is generally permitted to elevate its participation into an assignment only with the contemporaneous consent of the Eligible Borrower, the Eligible Lender and other necessary parties (i.e., the administrative agent in a multi-lender facility). However, the SPV may make certain transfers without such contemporaneous consent, including in the circumstances described above for elevation.

- Workouts. The SPV will rely on the Eligible Lender to service the loan prior to any workout situations. As long as the economic interests of the SPV and Eligible Lender are aligned, and the loan in question is not notably larger than the other loans in the SPV’s portfolio, the SPV would not be expected to elevate its participation. Instead, the SPV would be expected to rely on the Eligible Lender to follow market-standard workout processes and to exercise its standard of care. While Main Street loans are not forgivable, in the event of a workout, the SPV may agree to extended amortization schedules, reductions in interest (including capitalized interest) and priming loans.

- Pre-Funding vs. Conditional Funding. Eligible Lenders have the option to either (a) fund a Main Street loan first and then sell the participation to the SPV subsequently (which would require SPV approval), or (b) extend a Main Street loan contingent on a binding purchase commitment from the SPV.

Vedder Thinking | Articles Key Takeaways on Updated Main Street Lending Program Materials

Article

June 3, 2020

On May 27, 2020, the Federal Reserve Bank of Boston released updated Frequently Asked Questions (FAQs) and certain operational documents with respect to the Main Street Lending Program. The additional materials provide clarification on existing terms, add new requirements, include certain form documents to be used by borrowers and lenders, and give further guidance on the operation of the program. However, the FAQs and materials did not provide any form of loan application or timing of the program rollout.

Among the form documents are a Participation Agreement (which governs the purchase of the participation interest), Lender Registration Certifications and Covenants, a Servicing Agreement (which governs the administration of the participation and delivery of certain financial information), a Co-Lender Agreement (which would allow a bi-lateral facility to be converted into a multi-lender facility if there is an elevation of a participation interest), Lender Transaction Specific Certifications and Covenants, and Borrower Certifications and Covenants.

The updates expand the reach of the affiliation rules: affiliates of borrowers are now aggregated for purposes of (i) determining the Main Street loan facility that is available to a borrower, and (ii) the maximum loan size that a borrower may receive. Portfolio companies of private equity funds are not excluded from the Main Street Lending Program on a de facto basis. However, this expansion of the affiliation rules could impact the amount of Main Street loans that portfolio companies of private equity funds are able to receive.

Other notable changes are: (1) a no adequate credit available certification that is required from the borrower, (2) a new Collateral Coverage Ratio requirement for the Priority Loan Facility, (3) updated guidance on the security requirements for the Priority Loan Facility and Expanded Loan Facility, (4) clarifications on the methodology used to calculate EBITDA and permissible repayments of other debt, and (5) details on the rights the SPV will have via its participation, including specific voting rights and rights to elevate and/or transfer its participation.

The updated materials are available at the Federal Reserve Bank of Boston’s website by clicking here.

This bulletin briefly describes the key takeaways on the updated Main Street Lending Program materials. Alongside this bulletin, we have updated our easy-to-digest chart setting forth the high-level terms of the Main Street Lending Program. We note that this is current as of June 3, 2020 and adjustments to the program may be made in the future.

Click the image below to view the chart in full.

1. Expansion of Affiliation Rules: Affiliates will be aggregated with an Eligible Borrower not only for purposes of the maximum employee count (15,000) and maximum revenue ($5 billion) eligibility calculations, but now also will be aggregated for purposes of (i) determining the Main Street loan facility that is available to an Eligible Borrower, and (ii) the maximum loan size that an Eligible Borrower may receive.

- Available Loan Facility. An affiliated group of businesses can participate in only one Main Street facility, and cannot participate in both a Main Street facility and the Primary Market Corporate Credit Facility (PMCCF). For example, if an Eligible Borrower’s affiliate has participated in the New Loan Facility or has a pending application to participate in the New Loan Facility, then the Eligible Borrower would only be able to participate in the New Loan Facility and would be prohibited from participating in the Priority Loan Facility and Expanded Loan Facility.

- Maximum Loan Size. The maximum loan amounts that apply to an individual Eligible Borrower also apply to an Eligible Borrower and its affiliates in the aggregate. An Eligible Borrower’s maximum loan size is limited by its own leverage level, the leverage level of the affiliated group on a consolidated basis, and the size of any loan extended to other affiliates in the group. For example, in the case of the New Loan Facility, a potential borrower’s maximum loan amount would be the lesser of:

(a) $25 million (less any amount extended to an affiliate of the Eligible Borrower under the New Loan Facility);

(b) 4x 2019 adjusted EBITDA of the Eligible Borrower minus Eligible Borrower’s existing outstanding and undrawn available debt; and

(c) 4x 2019 adjusted EBITDA of the Eligible Borrower and its affiliates on a consolidated basis minus existing outstanding and undrawn available debt of the Eligible Borrower and its affiliates on a consolidated basis.

The affiliation test for maximum loan sizing purposes is the same one used for the maximum employee and revenue eligibility calculations. The affiliation test applies to private equity-owned businesses in the same manner as any other business subject to outside ownership or control. It is noted that the SBA affiliation exceptions in 13 CFR 121.103(b) apply to the Main Street Lending Program, including the exception for business concerns owned in whole or substantial part by investment companies licensed under the Small Business Investment Act of 1958, as amended.

VEDDER OBSERVATION: Although portfolio companies of private equity funds are not excluded from the Main Street Lending Program, this expansion of the affiliation rules could impact the amount of Main Street loans that portfolio companies of private equity funds are able to receive. However, we note that the Forms of Lender Transaction Specific Certifications and Covenants state that affiliates are included in loan sizing calculations “… if one or more of the Borrower’s affiliates previously participated, or has applied to participate, in the Facility ….” While the FAQs are not clear on this point, if a potential borrower’s affiliates have not applied for or participated in the Main Street Lending Program, then it is possible that affiliates need not be included in loan sizing calculations. Another open question is whether only those affiliates that apply for or participate in the Main Street Lending Program should be included in the loan sizing calculations (rather than all affiliates).

2. Other Eligibility Requirements:

- No Adequate Credit Elsewhere. The borrower must certify that it is unable to secure adequate credit accommodations from other banks. This does not necessarily mean that no other credit is available to the borrower, but can mean that the amount, price or terms of credit available from other sources are inadequate for the borrower’s needs during the current unusual and exigent circumstances. Borrowers are not required to demonstrate that applications for credit had been denied by other lenders or otherwise document that the amount, price or terms of credit available elsewhere are inadequate.

- Subsidiaries of Foreign Entities. A subsidiary of a foreign company can be eligible for a Main Street loan as long as the borrower itself has the required U.S. nexus. Loan proceeds may not be used for the benefit of foreign parents, affiliates or subsidiaries.

- Significant Operations. To determine if an Eligible Borrower has “significant operations” in the U.S., the business’s operations should be evaluated on a consolidated basis together with its subsidiaries, but not its parent companies or sister affiliates. For example, an Eligible Borrower has significant operations in the U.S. if, when consolidated with its subsidiaries, greater than 50% of the Eligible Borrower’s: (i) assets are located in the U.S.; (ii) annual net income is generated in the U.S.; (iii) annual net operating revenues are generated in the U.S.; or (iv) annual consolidated operating expenses (excluding interest expense and any other expenses associated with debt service) are generated in the U.S. This is a non-exhaustive list.

- Private Equity. While portfolio companies of private equity funds may be eligible for Main Street loans, private equity funds themselves are ineligible.

- Holding Companies. For holding companies, loan sizing calculations can be based on one or more operating subsidiaries selected by the borrower to provide a guarantee so long as each selected subsidiary is itself eligible under the Main Street Lending Program.

3. Expanded Loan Facility Updates:

- Eligible Lender Timing. The Eligible Lender is not required to have been the same Eligible Lender that originally extended the loan underlying an upsized tranche. However, the Eligible Lender must have purchased the interest in the underlying loan as of December 31, 2019, and the Eligible Lender must have assigned an internal risk rating to the underlying loan equivalent to a “pass” in the FFIEC’s supervisory rating system as of that date. Also, if an existing loan was originated after December 31, 2019, the Eligible Lender should use the internal risk rating given to that loan at origination to determine whether the loan is eligible for upsizing under the Expanded Loan program.

- 35% Prong of Loan Sizing Test. If the upsized tranche is part of a secured loan, then all secured debt for borrowed money that has not been made junior in priority through contractual subordination should be included in the 35% calculation regardless of value or type of collateral. If the upsized tranche is part of an unsecured loan, then all unsecured debt for borrowed money that has not been made junior in priority through contractual subordination should be included in the 35% calculation.

4. Priority Loan Facility Update:

- New Collateral Coverage Ratio Requirement. If the Priority Loan is secured, then the Collateral Coverage Ratio (i.e., the aggregate value of any relevant collateral, including the pro rata value of any Shared Collateral, divided by the outstanding aggregate principal amount of the relevant debt) for the Priority Loan at the time of its origination must be either (i) at least 200% or (ii) not less than the aggregate Collateral Coverage Ratio for all of the Borrower’s other secured Loans or Debt Instruments (other than mortgage debt).

5. Security Updates for Priority Loan Facility and Expanded Loan Facility:

- The Priority Loan and Expanded Loan must be secured if, at the time of origination, the Eligible Borrower has any other secured Loans or Debt Instruments (i.e., debt for borrowed money and all obligations evidenced by bonds, debentures, notes, loan agreements or other similar instruments, and all guarantees of the foregoing), other than mortgage debt.

- In the case of the Expanded Loan Facility, if the underlying credit facility includes both term loan tranche(s) and revolver tranche(s), the upsized tranche needs to share collateral on a pari passu basis with the term loan tranche(s) only.

- The lien of the Eligible Lender in any Shared Collateral (i.e., any collateral security for the eligible loan that is also collateral security for any of the borrower’s or guarantors’ other Loans or Debt Instruments (other than mortgage debt)) must be senior to or pari passu with the lien on Shared Collateral that secures any of the borrower’s other Loans or Debt Instruments (other than mortgage debt), including any other tranches in respect of the underlying loan in the case of the Expanded Loan Facility.

- The Priority Loan need not share in all of the collateral that secures the Eligible Borrower’s other Loans or Debt Instruments.

- The loan documents for the Priority Loan Facility and the Expanded Loan Facility must contain a lien covenant or negative pledge that is of the type – and contains exceptions, limitations, carve-outs, baskets, materiality thresholds, and qualifiers – that are consistent with those used by the Eligible Lender in its ordinary course lending to similarly situated borrowers. In the case of the Expanded Loan Facility, any lien covenant that was negotiated in good faith prior to April 24, 2020, as part of any underlying loan, is sufficient to satisfy this requirement.

6. EBITDA Calculations:

- If an Eligible Lender has used multiple EBITDA adjustment methods with respect to the Eligible Borrower or similarly situated borrowers (e.g., one for use within a credit agreement and one for internal risk management purposes), the Eligible Lender should choose the most conservative method (no cherry-picking), and must use a method used recently, but prior to April 24, 2020. The Eligible Lender should document the rationale for its selection of an adjusted EBITDA methodology.

- In the case of the Expanded Loan Facility, if EBITDA was not calculated or used when originating the loan underlying the upsized tranche, the Eligible Borrower’s adjusted EBITDA must be calculated using a methodology that the Eligible Lender has required to be used in other contexts for the Eligible Borrower or, if there is no such calculation, for similarly situated borrowers.

- Similarly situated borrowers are borrowers in similar industries with comparable risk and size characteristics. Eligible Lenders should document their process for identifying similarly situated borrowers when they originate a New Loan or Priority Loan.

7. Fees: Eligible Lenders are not permitted to charge Eligible Borrowers any additional fees beyond the fees described in the Main Street Lending Program, except de minimis fees for services that are customary and necessary, such as appraisal and legal fees. Eligible Lenders should not charge servicing fees to Eligible Borrowers.

8. Loan Documentation:Eligible Lenders should use their own standard loan documents which should be substantially similar (except for necessary changes to accommodate the requirements of the Main Street Lending Program), including with respect to covenants, to the loan documents used in its ordinary course lending to similarly situated borrowers (in terms of industry and risk and size characteristics). There are certain covenants that are required to be included in the loan documents, including with respect to mandatory prepayments, cross-acceleration and financial reporting (samples of which have been provided).

9. Repayments:

- Repaying Other Debt. Eligible Borrowers are generally prohibited from repaying other debt until the Main Street loan is repaid in full, unless the principal or interest payment is “mandatory and due,” meaning (a) on the future date upon which they were scheduled to be paid as of April 24, 2020 or (b) upon the occurrence of an event that automatically triggers mandatory prepayments under a contract for indebtedness that the Eligible Borrower executed prior to April 24, 2020, except that any such prepayments triggered by the incurrence of new debt can only be paid if they are de minimis or, in the case of Priority Loans, at the time of origination.

- Mandatory Prepayment of Existing Debt. If an Eligible Borrower has an existing debt arrangement that requires prepayment of more than a de minimis amount upon the incurrence of new debt, the Eligible Borrower cannot receive a New Loan or Expanded Loan unless such requirement is waived or reduced to a de minimis amount by the relevant creditor.

10. SPV Participation:

- Voting. The SPV will have voting rights with respect to items that are customary “sacred rights” and certain other items that are specific to the Main Street Lending Program, such as waivers of conditions precedent to closing, amendments to certain borrower eligibility certifications and covenants, amendments to certain periodic financial reporting, greater restrictions on lender assignability, adverse effect on participated loans that would be disproportionate, and certain actions relating to the required cross-acceleration provisions.

- Elevation of SPV Participation. The SPV can generally elevate its participation in the loan into an assignment without the consent of the Eligible Lender and Eligible Borrower in the following circumstances: (i) if the Eligible Borrower fails to make a payment and the applicable grace period expires; (ii) if the Eligible Borrower or Eligible Lender is subject to bankruptcy or insolvency proceedings; (iii) automatically, if the Eligible Lender would allow any portion of the underlying loan to be forgiven; and (iv) if required by law.

- Sale of SPV Participation. The SPV is generally permitted to sell its participation (without elevating) only with the contemporaneous consent of the Eligible Lender. In addition, it is generally permitted to elevate its participation into an assignment only with the contemporaneous consent of the Eligible Borrower, the Eligible Lender and other necessary parties (i.e., the administrative agent in a multi-lender facility). However, the SPV may make certain transfers without such contemporaneous consent, including in the circumstances described above for elevation.

- Workouts. The SPV will rely on the Eligible Lender to service the loan prior to any workout situations. As long as the economic interests of the SPV and Eligible Lender are aligned, and the loan in question is not notably larger than the other loans in the SPV’s portfolio, the SPV would not be expected to elevate its participation. Instead, the SPV would be expected to rely on the Eligible Lender to follow market-standard workout processes and to exercise its standard of care. While Main Street loans are not forgivable, in the event of a workout, the SPV may agree to extended amortization schedules, reductions in interest (including capitalized interest) and priming loans.

- Pre-Funding vs. Conditional Funding. Eligible Lenders have the option to either (a) fund a Main Street loan first and then sell the participation to the SPV subsequently (which would require SPV approval), or (b) extend a Main Street loan contingent on a binding purchase commitment from the SPV.