SEC Proposes Significant Money Market Fund Reforms

Seeking to address issues experienced by certain money market funds in March 2020, at the onset of the COVID-19 pandemic, the SEC recently proposed significant and expansive money market fund reforms. The SEC’s multi-faceted proposal, approved on December 15, 2021 by a three-to-two vote, would amend Rule 2a-7 under the Investment Company Act of 1940 to, among other things: increase daily and weekly liquid asset requirements for all money market funds (MMFs); modify stress testing requirements; require MMFs to calculate their “dollar-weighted average portfolio maturity” (WAM) and “dollar-weighted average life maturity” (WAL) using the market values of their portfolio securities; remove liquidity fee and redemption gate provisions from Rule 2a-7; and impose a new swing pricing regime for non-government institutional money market funds (i.e., institutional prime and institutional tax-exempt MMFs). The proposed reforms impose certain new requirements on MMF boards of directors, including the independent directors, which are described below.

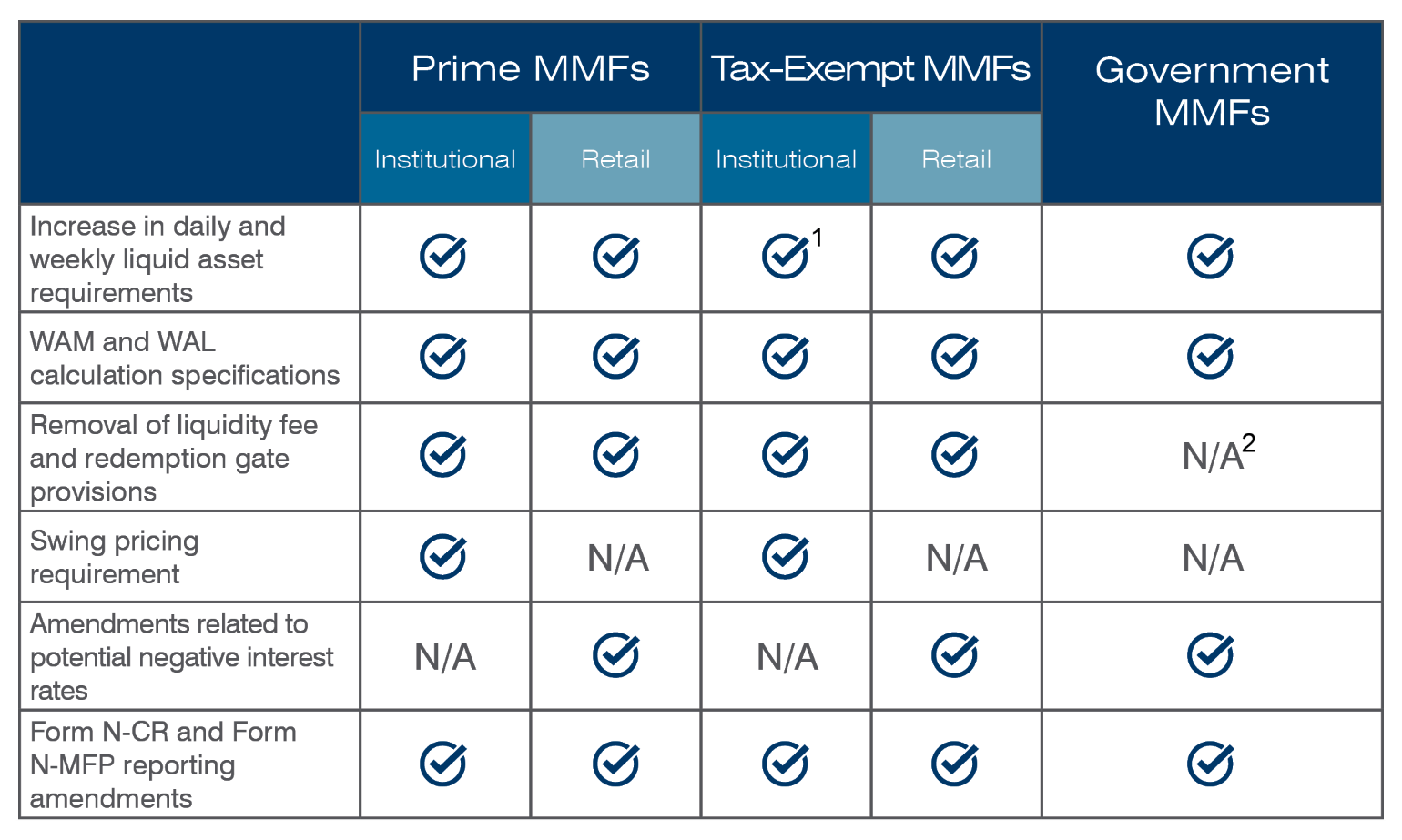

Overview - Applicability of Reform Components to MMFs:

- Increase in Daily and Weekly Liquid Asset Minimums. In order to provide a more substantial liquidity buffer in the event of rapid redemptions, a MMF’s minimum liquid asset requirements would increase from 10% daily liquid assets to 25%, and from 30% weekly liquid assets to 50%.

- New Board Notification. The proposal would require notifications to the MMF board upon the occurrence of specific liquidity threshold events. Specifically, a MMF would be required to notify its board when the fund has invested less than 12.5% of its total assets in daily liquid assets or less than 25% of its total assets in weekly liquid assets (i.e., when the fund experiences a greater than 50% decrease in liquidity below at least one of the proposed daily and weekly liquid asset requirements) (a liquidity threshold event).

- - Following a liquidity threshold event, the proposal would require a MMF (i) to notify the board within one business day of the liquidity threshold event and (ii) to provide the board with a brief description of the facts and circumstances that led to the liquidity threshold event within four business days of the event.

- The proposal does not contemplate any specific action to be taken by the board upon receipt of such notification.

- - Following a liquidity threshold event, the proposal would require a MMF (i) to notify the board within one business day of the liquidity threshold event and (ii) to provide the board with a brief description of the facts and circumstances that led to the liquidity threshold event within four business days of the event.

- Modifications to Liquidity Stress Testing Requirements. The proposed reforms would eliminate stress testing at the current 10% weekly liquid asset level, and instead, a MMF would be required to determine the minimum level of liquidity it seeks to maintain during stress periods, periodically test its ability to maintain such liquidity, and provide the board with a report on the results of such testing.

- New Board Notification. The proposal would require notifications to the MMF board upon the occurrence of specific liquidity threshold events. Specifically, a MMF would be required to notify its board when the fund has invested less than 12.5% of its total assets in daily liquid assets or less than 25% of its total assets in weekly liquid assets (i.e., when the fund experiences a greater than 50% decrease in liquidity below at least one of the proposed daily and weekly liquid asset requirements) (a liquidity threshold event).

- WAM and WAL Calculation Specifications. The proposal would require that MMFs calculate WAM and WAL based on the percentage of each security’s market value in a fund’s portfolio.

- This reform would prohibit the practice of calculating WAM and WAL using the amortized cost of each portfolio security.

- Elimination of Liquidity Fees and Redemption Gates. The provisions of Rule 2a-7 that were added in the 2014 MMF rule amendments to permit liquidity fees and redemption gates (and sometimes require liquidity fees) when a MMF’s weekly liquid assets fall below certain thresholds would be removed.

- The SEC observed that the possibility of fees and/or gates being imposed appeared to contribute to investors’ incentives to redeem from prime MMFs in March 2020 as some funds’ liquidity levels declined.

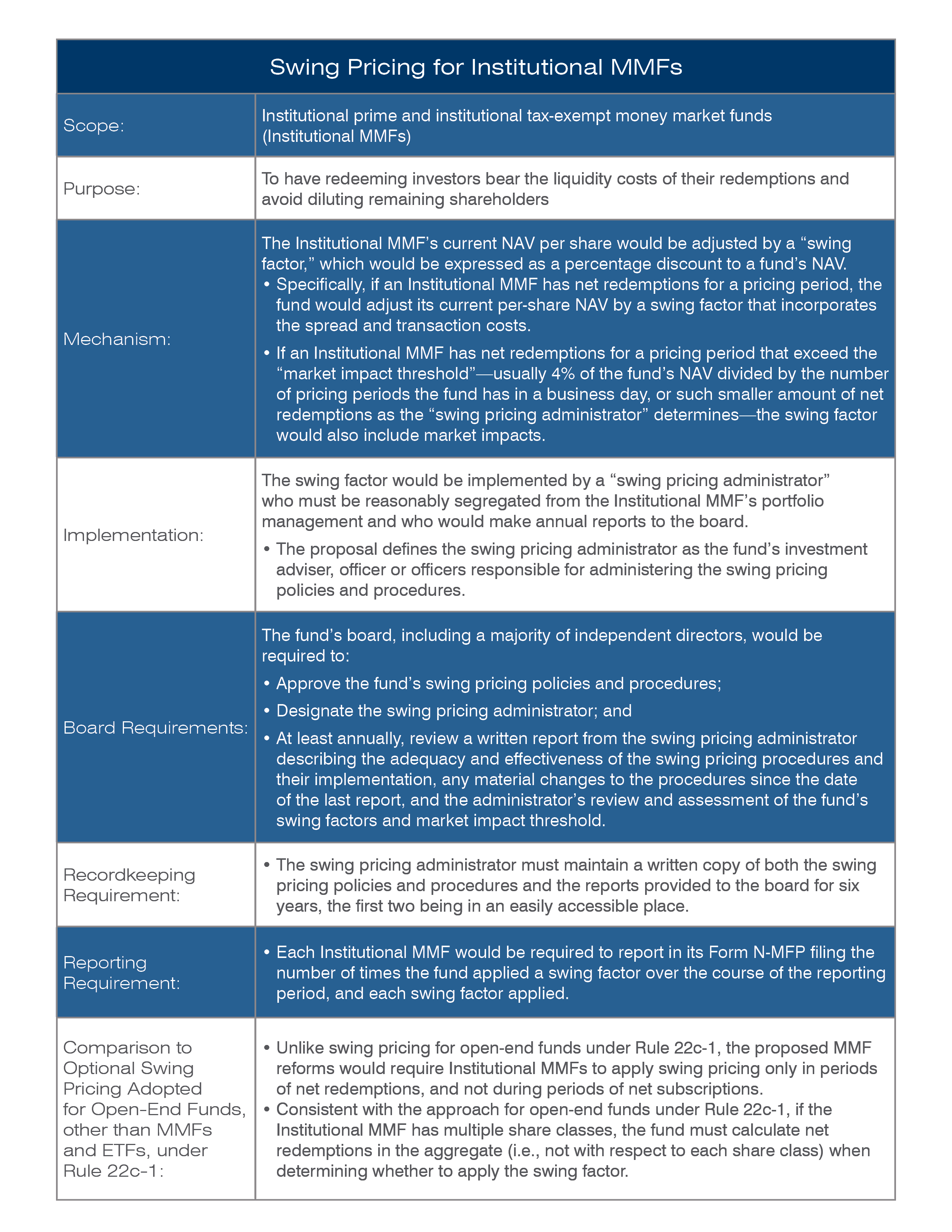

- Imposition of Swing Pricing Requirement for Institutional MMFs. The proposal would require institutional MMFs to adopt swing pricing procedures to adjust a fund’s current NAV per share by a “swing factor” that effectively passes portfolio transaction costs stemming from shareholder redemptions (but not subscriptions) on to the redeeming shareholders, instead of the transaction costs being borne by the fund’s remaining shareholders. The swing factor would be applied when the fund has net redemptions during a “pricing period” (i.e., the period between the fund’s NAV strikes for shareholder transactions). Additional elements of the swing pricing requirement are summarized in the table below.

- Amendments Related to Potential Negative Interest Rates. Rule 2a-7 currently allows retail MMFs to use amortized cost and penny-rounding to seek to maintain a stable $1.00 NAV, provided that the fund’s board believes such pricing fairly reflects the fund’s market-based NAV. The SEC’s proposing release for the latest MMF reforms acknowledges that Rule 2a-7 currently does not explicitly address how MMFs must operate when interest rates are negative. The proposing release states that if interest rates turn negative, “the board of a stable NAV fund could reasonably require the fund to convert to a floating share price to prevent material dilution or other unfair results to investor or current shareholders.”

- The proposal includes amendments to help assure the operation of government or retail stable NAV funds that have converted to a floating share price due to negative interest rates.

- Prohibition of “Reverse Distribution Mechanisms.” The proposal would amend Rule 2a-7 to prohibit MMFs from utilizing a “reverse distribution mechanism” whereby a fund reduces the number of its outstanding shares to maintain a stable NAV despite a negative interest rate environment.

- Reporting Requirements. The proposal would amend existing, and impose new, reporting requirements on Forms N-MFP and N-CR, and would also make certain conforming changes to Form N-1A.

- Form N-CR. The proposal would require MMFs to file reports on Form N-CR in a custom structured data format—XML—and make certain other reporting modifications, such as by removing the reporting events that relate to liquidity fees and redemption gates. Liquidity threshold events reported to the board would also need to be reported on Form N-CR.

- Form N-MFP. Proposed amendments to Form N-MFP would include various new disclosure requirements that vary depending on the type of MMF and pertaining to the composition and concentration of the fund’s shareholders, portfolio securities sold and imposition of swing pricing during the reporting period.

- Form N-1A. The proposal would require Institutional MMFs to: (i) include a general description of the effects of swing pricing on the fund’s annual total returns as a footnote to its risk/return bar chart and table; (ii) include a description of swing pricing in its disclosure regarding procedures for pricing fund shares; and (iii) explain the fund’s use of swing pricing, including its meaning, the circumstances under which the fund will use it, and the effects of swing pricing on the fund and investors.

- Compliance Dates. The SEC is proposing that removal of the liquidity fees and redemption gates provisions take effect upon the effective date of the final rule. The SEC is proposing the following transition periods, after the effective date of the final rule, for compliance with the remainder of the proposed money market fund rule amendments: (i) a 12-month transition period for the swing pricing requirements, and (ii) a six-month transition period for all other aspects of the proposal.

Comments on the proposal will be due 60 days after publication in the Federal Register. The SEC’s proposing release is available here.

Vedder Thinking | Articles SEC Proposes Significant Money Market Fund Reforms

Article

February 10, 2022

Seeking to address issues experienced by certain money market funds in March 2020, at the onset of the COVID-19 pandemic, the SEC recently proposed significant and expansive money market fund reforms. The SEC’s multi-faceted proposal, approved on December 15, 2021 by a three-to-two vote, would amend Rule 2a-7 under the Investment Company Act of 1940 to, among other things: increase daily and weekly liquid asset requirements for all money market funds (MMFs); modify stress testing requirements; require MMFs to calculate their “dollar-weighted average portfolio maturity” (WAM) and “dollar-weighted average life maturity” (WAL) using the market values of their portfolio securities; remove liquidity fee and redemption gate provisions from Rule 2a-7; and impose a new swing pricing regime for non-government institutional money market funds (i.e., institutional prime and institutional tax-exempt MMFs). The proposed reforms impose certain new requirements on MMF boards of directors, including the independent directors, which are described below.

Overview - Applicability of Reform Components to MMFs:

- Increase in Daily and Weekly Liquid Asset Minimums. In order to provide a more substantial liquidity buffer in the event of rapid redemptions, a MMF’s minimum liquid asset requirements would increase from 10% daily liquid assets to 25%, and from 30% weekly liquid assets to 50%.

- New Board Notification. The proposal would require notifications to the MMF board upon the occurrence of specific liquidity threshold events. Specifically, a MMF would be required to notify its board when the fund has invested less than 12.5% of its total assets in daily liquid assets or less than 25% of its total assets in weekly liquid assets (i.e., when the fund experiences a greater than 50% decrease in liquidity below at least one of the proposed daily and weekly liquid asset requirements) (a liquidity threshold event).

- - Following a liquidity threshold event, the proposal would require a MMF (i) to notify the board within one business day of the liquidity threshold event and (ii) to provide the board with a brief description of the facts and circumstances that led to the liquidity threshold event within four business days of the event.

- The proposal does not contemplate any specific action to be taken by the board upon receipt of such notification.

- - Following a liquidity threshold event, the proposal would require a MMF (i) to notify the board within one business day of the liquidity threshold event and (ii) to provide the board with a brief description of the facts and circumstances that led to the liquidity threshold event within four business days of the event.

- Modifications to Liquidity Stress Testing Requirements. The proposed reforms would eliminate stress testing at the current 10% weekly liquid asset level, and instead, a MMF would be required to determine the minimum level of liquidity it seeks to maintain during stress periods, periodically test its ability to maintain such liquidity, and provide the board with a report on the results of such testing.

- New Board Notification. The proposal would require notifications to the MMF board upon the occurrence of specific liquidity threshold events. Specifically, a MMF would be required to notify its board when the fund has invested less than 12.5% of its total assets in daily liquid assets or less than 25% of its total assets in weekly liquid assets (i.e., when the fund experiences a greater than 50% decrease in liquidity below at least one of the proposed daily and weekly liquid asset requirements) (a liquidity threshold event).

- WAM and WAL Calculation Specifications. The proposal would require that MMFs calculate WAM and WAL based on the percentage of each security’s market value in a fund’s portfolio.

- This reform would prohibit the practice of calculating WAM and WAL using the amortized cost of each portfolio security.

- Elimination of Liquidity Fees and Redemption Gates. The provisions of Rule 2a-7 that were added in the 2014 MMF rule amendments to permit liquidity fees and redemption gates (and sometimes require liquidity fees) when a MMF’s weekly liquid assets fall below certain thresholds would be removed.

- The SEC observed that the possibility of fees and/or gates being imposed appeared to contribute to investors’ incentives to redeem from prime MMFs in March 2020 as some funds’ liquidity levels declined.

- Imposition of Swing Pricing Requirement for Institutional MMFs. The proposal would require institutional MMFs to adopt swing pricing procedures to adjust a fund’s current NAV per share by a “swing factor” that effectively passes portfolio transaction costs stemming from shareholder redemptions (but not subscriptions) on to the redeeming shareholders, instead of the transaction costs being borne by the fund’s remaining shareholders. The swing factor would be applied when the fund has net redemptions during a “pricing period” (i.e., the period between the fund’s NAV strikes for shareholder transactions). Additional elements of the swing pricing requirement are summarized in the table below.

- Amendments Related to Potential Negative Interest Rates. Rule 2a-7 currently allows retail MMFs to use amortized cost and penny-rounding to seek to maintain a stable $1.00 NAV, provided that the fund’s board believes such pricing fairly reflects the fund’s market-based NAV. The SEC’s proposing release for the latest MMF reforms acknowledges that Rule 2a-7 currently does not explicitly address how MMFs must operate when interest rates are negative. The proposing release states that if interest rates turn negative, “the board of a stable NAV fund could reasonably require the fund to convert to a floating share price to prevent material dilution or other unfair results to investor or current shareholders.”

- The proposal includes amendments to help assure the operation of government or retail stable NAV funds that have converted to a floating share price due to negative interest rates.

- Prohibition of “Reverse Distribution Mechanisms.” The proposal would amend Rule 2a-7 to prohibit MMFs from utilizing a “reverse distribution mechanism” whereby a fund reduces the number of its outstanding shares to maintain a stable NAV despite a negative interest rate environment.

- Reporting Requirements. The proposal would amend existing, and impose new, reporting requirements on Forms N-MFP and N-CR, and would also make certain conforming changes to Form N-1A.

- Form N-CR. The proposal would require MMFs to file reports on Form N-CR in a custom structured data format—XML—and make certain other reporting modifications, such as by removing the reporting events that relate to liquidity fees and redemption gates. Liquidity threshold events reported to the board would also need to be reported on Form N-CR.

- Form N-MFP. Proposed amendments to Form N-MFP would include various new disclosure requirements that vary depending on the type of MMF and pertaining to the composition and concentration of the fund’s shareholders, portfolio securities sold and imposition of swing pricing during the reporting period.

- Form N-1A. The proposal would require Institutional MMFs to: (i) include a general description of the effects of swing pricing on the fund’s annual total returns as a footnote to its risk/return bar chart and table; (ii) include a description of swing pricing in its disclosure regarding procedures for pricing fund shares; and (iii) explain the fund’s use of swing pricing, including its meaning, the circumstances under which the fund will use it, and the effects of swing pricing on the fund and investors.

- Compliance Dates. The SEC is proposing that removal of the liquidity fees and redemption gates provisions take effect upon the effective date of the final rule. The SEC is proposing the following transition periods, after the effective date of the final rule, for compliance with the remainder of the proposed money market fund rule amendments: (i) a 12-month transition period for the swing pricing requirements, and (ii) a six-month transition period for all other aspects of the proposal.

Comments on the proposal will be due 60 days after publication in the Federal Register. The SEC’s proposing release is available here.