SEC Adopts Significant Amendments to Beneficial Ownership Reporting Requirements

On October 10, 2023, the SEC adopted significant amendments to the rules governing beneficial ownership reporting, including accelerated filing deadlines for Schedules 13D and 13G filers.

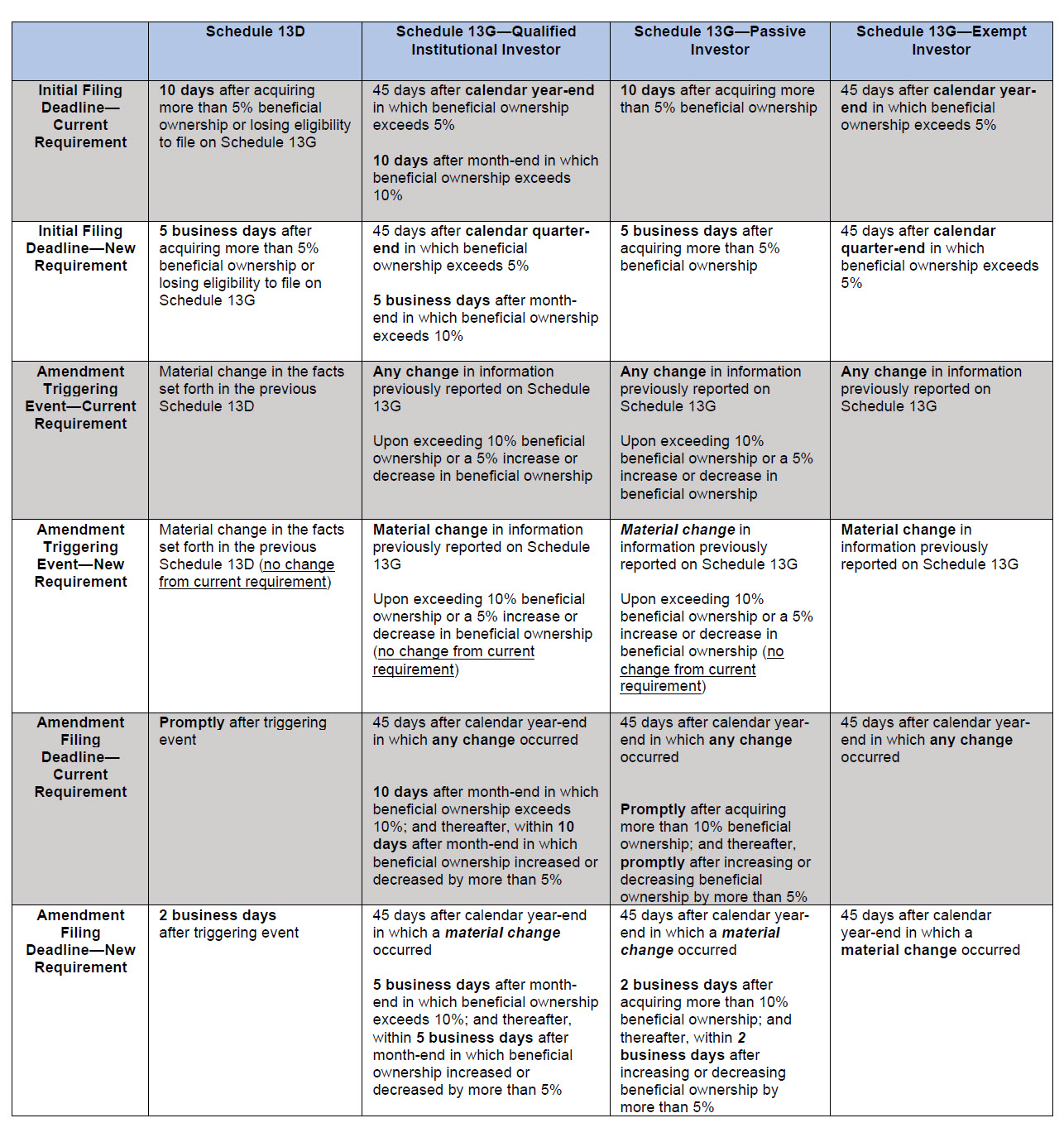

The following table compares the current and new filing deadlines, including certain differences in requirements among Qualified Institutional Investors, passive investors and exempt investors, as well as amendment triggering events and deadlines for such amendment filings.

Other Elements of the Amendments and the SEC’s Adopting Release

- Extended Filing Cut-off Times. To accommodate the accelerated filing deadlines, cut-off times for Schedule 13D and 13G filings are extended from 5:30 p.m. to 10:00 p.m. ET.

- Guidance on “Group” Beneficial Ownership. Rather than adopting certain proposed amendments to Rule 13d-5(b), the SEC included guidance in the adopting release regarding the appropriate legal standard for determining whether a “group” is formed for purposes of the reporting requirements. Among other things, the SEC noted that the determination depends on an analysis of all relevant facts and circumstances and not solely on the presence or absence of an express agreement, and that the evidence must show, at a minimum, indicia, such as an informal arrangement or coordination in furtherance of, a common purpose to acquire, hold or dispose of securities of an issuer. Shareholder engagement activities involving discussions and exchanging views, without other actions, would not constitute formation of a group. Similarly, the adopting release states that when shareholders jointly make recommendations to an issuer regarding the structure and composition of the issuer’s board of directors that do not involve attempts to convince the board to take specific actions through a change in the existing board membership or bind the board to take action, the SEC does not believe a group is formed.

- Guidance on Beneficial Ownership through Cash-Settled Derivative Securities. As with proposed amendments regarding formation of a group, the SEC, rather than adopting proposed rule amendments, included guidance in the adopting release about circumstances in which a holder of a cash-settled derivative security, other than a security-based swap,

may be deemed the beneficial owner of the reference security. According to the SEC’s guidance, such circumstances include when:

- the derivative provides the holder with exclusive or shared voting or investment power through a contractual term or otherwise;

- the derivative is acquired in order to divest the holder of beneficial ownership of the security or to prevent the vesting of that beneficial ownership as part of a plan or scheme to evade the reporting requirements; or

- under the terms of the derivative or an understanding related to it, the holder has a right to acquire beneficial ownership of the security within 60 days or acquires the right to acquire beneficial ownership of the reference security with control purpose, regardless of when the right is exercisable.

- Amendment to Item 6 of Schedule 13D. To further clarify the disclosure requirements with respect to derivative securities, the amendments revise Item 6 of Schedule 13D to remove any implication that a person is not required to disclose interests in all derivative securities (including cash-settled derivatives) that use a covered class as a reference security. The adopting release notes that a derivative security need not have originated with the issuer, or otherwise be part of the issuer’s capital structure, in order for an Item 6 disclosure obligation to arise.

- Structured Data Requirement. The amendments require that Schedule 13D and 13G filings (other than exhibits) be made using a structured, machine-readable data language.

The amendments related to Schedule 13D (except the structured data language requirement) and the extension of the filing cut-off time will be effective on February 5, 2024. Compliance with the revised Schedule 13G filing deadlines will be required as of September 30, 2024.The revised structured data requirements for Schedules 13D and 13G will be effective on December 18, 2024.

The SEC’s adopting release is available here, a related fact sheet is available here, and a related press release is available here.

Vedder Thinking | Articles SEC Adopts Significant Amendments to Beneficial Ownership Reporting Requirements

Article

November 22, 2023

On October 10, 2023, the SEC adopted significant amendments to the rules governing beneficial ownership reporting, including accelerated filing deadlines for Schedules 13D and 13G filers.

The following table compares the current and new filing deadlines, including certain differences in requirements among Qualified Institutional Investors, passive investors and exempt investors, as well as amendment triggering events and deadlines for such amendment filings.

Other Elements of the Amendments and the SEC’s Adopting Release

- Extended Filing Cut-off Times. To accommodate the accelerated filing deadlines, cut-off times for Schedule 13D and 13G filings are extended from 5:30 p.m. to 10:00 p.m. ET.

- Guidance on “Group” Beneficial Ownership. Rather than adopting certain proposed amendments to Rule 13d-5(b), the SEC included guidance in the adopting release regarding the appropriate legal standard for determining whether a “group” is formed for purposes of the reporting requirements. Among other things, the SEC noted that the determination depends on an analysis of all relevant facts and circumstances and not solely on the presence or absence of an express agreement, and that the evidence must show, at a minimum, indicia, such as an informal arrangement or coordination in furtherance of, a common purpose to acquire, hold or dispose of securities of an issuer. Shareholder engagement activities involving discussions and exchanging views, without other actions, would not constitute formation of a group. Similarly, the adopting release states that when shareholders jointly make recommendations to an issuer regarding the structure and composition of the issuer’s board of directors that do not involve attempts to convince the board to take specific actions through a change in the existing board membership or bind the board to take action, the SEC does not believe a group is formed.

- Guidance on Beneficial Ownership through Cash-Settled Derivative Securities. As with proposed amendments regarding formation of a group, the SEC, rather than adopting proposed rule amendments, included guidance in the adopting release about circumstances in which a holder of a cash-settled derivative security, other than a security-based swap,

may be deemed the beneficial owner of the reference security. According to the SEC’s guidance, such circumstances include when:

- the derivative provides the holder with exclusive or shared voting or investment power through a contractual term or otherwise;

- the derivative is acquired in order to divest the holder of beneficial ownership of the security or to prevent the vesting of that beneficial ownership as part of a plan or scheme to evade the reporting requirements; or

- under the terms of the derivative or an understanding related to it, the holder has a right to acquire beneficial ownership of the security within 60 days or acquires the right to acquire beneficial ownership of the reference security with control purpose, regardless of when the right is exercisable.

- Amendment to Item 6 of Schedule 13D. To further clarify the disclosure requirements with respect to derivative securities, the amendments revise Item 6 of Schedule 13D to remove any implication that a person is not required to disclose interests in all derivative securities (including cash-settled derivatives) that use a covered class as a reference security. The adopting release notes that a derivative security need not have originated with the issuer, or otherwise be part of the issuer’s capital structure, in order for an Item 6 disclosure obligation to arise.

- Structured Data Requirement. The amendments require that Schedule 13D and 13G filings (other than exhibits) be made using a structured, machine-readable data language.

The amendments related to Schedule 13D (except the structured data language requirement) and the extension of the filing cut-off time will be effective on February 5, 2024. Compliance with the revised Schedule 13G filing deadlines will be required as of September 30, 2024.The revised structured data requirements for Schedules 13D and 13G will be effective on December 18, 2024.

The SEC’s adopting release is available here, a related fact sheet is available here, and a related press release is available here.

Professionals

-

Services